My micro-acquisition process from first-touch to close & asset transfer — Part 2

Computing cash-on-cash, compiling research into an offer, financing options, LOI submissions & closing the deal

It’s relatively straightforward to identify whether a deal is qualitatively good because you have already have clarity on what kind of products you are looking for.

Quantifying whether a deal is worth investing into is a totally different exercise that is much more science than it is art.

Because I have a clear fund goal to return 2.7x over 2 years, one of the easiest ways to ensure its success is by computing what my returns must be from each deal so that my aggregate return works.

Consider a given opportunity expected to produce a 2.2x multiple on invested capital (MOIC) over 2 years on the basis of its EOY2 ARR, additionally delivering “only” 56% cash-on-cash (vs the required 70%) over the 2 years.

I may be willing to forego the MRR gap knowing the product is going to be worth much more, and that I’ll make it up at exit, later on.

This is a computation, so you need to build a calculator for yourself that helps quantify whether a given investment scenario is going to produce the expected goals you’ve set to accomplish.

Once you have a general idea of what your offer range is, the next thing you want to figure out is how to execute the transaction.

This means the other side of that coin is the method by which you intend to complete your transaction, and the second-order consequences you’ll incur from using such financing mechanisms.

You’re building scenarios to know how each one works out, so you need some inputs relative to your offer, unit economics and financing mechanisms so you can find your year-on-year outputs.

Where part 1 of the process is concerned with finding opportunities, part 2 aims to close deals with a high confidence of success both from a transactional perspective but also to increase the rate of return on invested cash.

Build a pro forma of the acquisition terms and determine possible financing scenarios based on my available capital

Now that you know the expected earnings of the product you’re analyzing and your general offer range, you can begin to orchestrate various combinations to finance the acquisition in a way that creates the highest return for your effort.

The valuation of the product will be driven by its ARR.

You can create a pretty standard spreadsheet whereby the main inputs are unit economics + the current EBIT + your expected offer range which would have already been established by now.

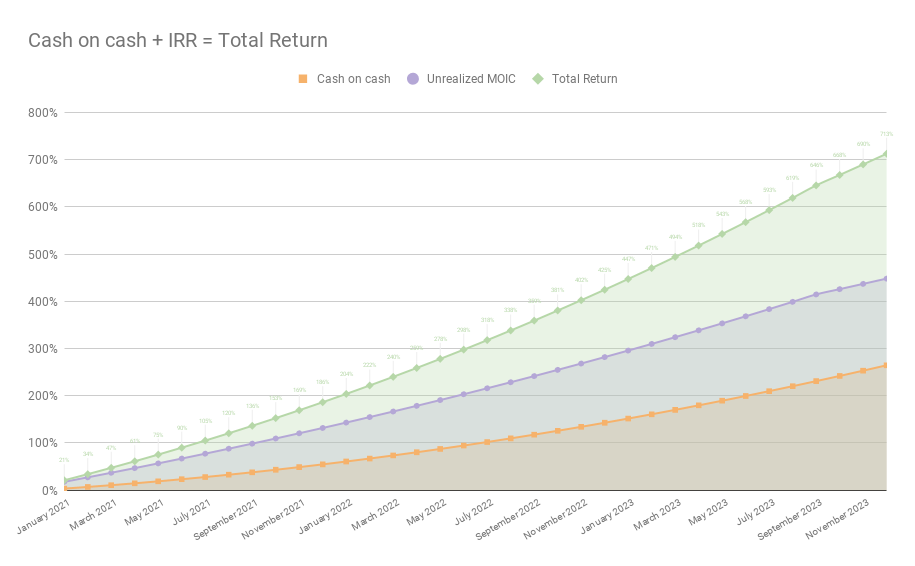

Reconcilely is due to hit 2.7x by May 2022 Because I’m aiming for all-cash transactions, that’s where I start. My sheet supports cash balances and loans, but I can set those to 0 and assume I’ll pay the whole thing all-cash.

This sheet outputs the expected 3-7 year performance assuming the current revenue growth rate, which I will also have quantified by now.

I can then discount costs and taxes and get a general idea of what my cash-on-cash returns will be on any given year.

Because I can realistically chart the ARR growth, I can also derive a valuation for the assets on that basis, typically applying multiples that follow my own benchmarks as a buyer.

Confirm minimum-return scenario for 2.7x

With the expected end of year valuation for each product, I can also get a decent picture of my rate of return at the end of each year, provided I would sell off the asset.

Then, I can simply add the total cash-on-cash over two years plus the valuation increase and check whether I’m over or under a 270% total return on my invested capital by fund close.

Explore other financing scenarios

Obviously, all-cash isn’t possible for everyone. There are plenty of deals I can’t buy all-cash, and that number increases as my available funds decrease, too.

Let’s assume I want to make an offer to acquire something for $500K that is generating $15K MRR, and that’s the expected offer I want to make.

At this point in time, and provided I don’t inject any more funds into MicroAngel, there’s $350k left for me to invest.

The math doesn’t work for all-cash, which then introduces many other possibilities from here. The goal is to be creative.

What if I introduce a cash balance? What about a lender?

As you adjust inputs, your cash-on-cash returns will change as they’re directly impacted by the other financial instruments used in the transaction, namely, debt service.

If the profit margin of the product is strong at 95%, the yearly earnings would be approximately (15,000 * 12 * 0.95) $171k.

Using a cash balance in this case would be very aggressive and apply huge pressure on cash flows, thereby decreasing the cash-on-cash returns

I’d have to hold + work on the product without any cash-on-cash over the whole first year. Not really what I’m looking for.

Also, the expected valuation path of the company given its current growth rate is not expected to yield a 2x return in 2 years.

In this case, one might aim to extend the cash balance from 12 months to 24 months, decreasing payments from $12.5k/mo to $6.25k/mo:

Unfortunately, this still doesn’t produce the results we’re looking for. The cash balance impact on the cash flows is too severe to perceive a 70% cash-on-cash return, and the ARR growth isn’t strong enough to justify a 2x MOIC.

What if, instead of using a cash balance, I orchestrate a small loan of $150k to service the rest of the transaction?

With a typical 7 year loan, the impact on take-home cash-on-cash is spread out over a much longer period of time.

In fact, as the product revenue grows, the debt service becomes less and less of a relevant burden relative the total budget, and increases the cash-on-cash rate of growth over time.

In this case, the EOY2 total cash-on-cash is bang on at 70%, but the valuation will still have grown too slowly to justify a 2x return.

In this case, I’d basically be getting my $350k back at the end of 2 years, with the benefit of having perceived a 2-year 70% cash-on-cash return on my investment.

That’s pretty awesome, but still off-target for my own devices.

Herein lies the difficulty of building a cashflow-based business with debt: the debt applies a ceiling to your profit that cannot be cancelled out without increasing revenue.

By the time you’ve identified a few scenarios that fit, you’ll be in a position to choose the combination of financing methods that produce the highest return given your offer and expected revenue outcomes.

It’s worth mentioning that the amount of time you’ll spend doing this exercise will dramatically decrease over time due to your ability to quickly pattern find what kind of deals are within your scope granted the financial vehicles at your disposal.

As you recognize your own limits for financing, that will draw boundaries for what kind of deals you can afford to acquire.

Once you’re set on your financing, you can move on to the LOI.

Write up an initial LOI containing the up-front consideration and terms

The purpose of (non-binding) letters of intent is to make an official statement of intent to acquire the company under certain terms, and propose the high level agreement by which such terms will come to fruition.

The main purpose of the LOI is to formalize exploratory dialogue into deliberate process, with the short-term goal to produce a more expansive purchase agreement to govern the eventual transaction.

→ Download the MicroAngel LOI Template (Subscribers Only)

If you’re going to use a combination of financing instruments, the LOI is the first place where you’ll define those.

Your LOI doesn’t need to be longer than like, 5 pages of legalese.

It should also include a baked-in non-disclosure agreement that protects the information shared in the scope of the transaction, and how such information should be disposed of in the event both parties choose to part ways.

Send LOI via PandaDoc

I’ve been using PandaDoc for sending and signing digital documents lately, but any similar solution (open source or otherwise) will do the trick.

Don’t send PDFs that people need to print and sign and scan. Just don’t do that. It’s 2021, use digital signatures.

Review LOI with seller and adjust if necessary

Most sellers will sign an LOI up-front. A small percentage will send it to a lawyer. I usually see that as a yellow flag.

Someone who keeps your LOI for more than 48 hours exposes you to being outbid by another buyer who will have a clear number to beat in order to secure the transaction.

Once an LOI is submitted, it is in the best interest of the seller to shop around and try to get someone to match and/or beat that offer for the most optimized outcome.

Don’t do that to yourself.

I expire my LOIs after 24 hours. If you and I are going to have a real conversation, you should be able to sign my human-readable letter and kickoff due diligence immediately.

Someone who’s serious about a deal signs an LOI very quickly. You don’t need a lawyer for that because it’s non-binding anyway. But that’s just my opinion. There will be hecklers.

Review financing components with seller if necessary

Before signing the LOI, the seller might have questions about how the transaction will take place, especially if you include a cash balance or an extended payment plan, or worse, a buyout.

This is a crucial juncture where the risk of the deal disintegrating is at its highest. There is usually quite a bit of apathy and disregard for the buyer’s circumstance.

The seller has a clear idea of what they’re willing to accept and not accept on the basis of what their perceived worth is.

If you fail to meet that expectation with terms that are too aggressive, there is a risk of the seller fully disconnecting from the idea of selling altogether, for fear that it will lead to a complicated process before they can see their money.

Or, more classically, they may choose to withdraw their interest to sell altogether hoping to achieve a higher valuation later on. This is the worst outcome for me.

You’d be surprised how often I lose deals to that psychology.

If I have a decent expectation to use a lender and/or a cash balance (or anything else), I mention it very early in the exploration process, typically during the Zoom meet and greet.

This way, the conversation can begin from a place of mutual scopes, where both parties try to figure out if those scopes align well enough to make a transaction possible.

For the vast majority of sellers, a cash balance is probably the thing they will be most comfortable with. People don’t mind deferring being paid, especially if a small bonus is attached.

Since liquidity events for self employed individuals are few and far between, those individuals will often optimize for a higher total sum, even if a percentage of that sum is deferred to a later date.

Like product pricing, the ceiling of what you can do is what your customer is willing to accept. The floor is what you have no choice but to start with (hard limits, costs).

Received signed LOI

Congratulations! You’ve received a worthless piece of paper back from the seller. An LOI is non-binding.

You have nothing yet. All you have is formalized interest. You have figured out a context by which someone will agree to let go of their company and give it to you.

This is the outcome you want, since the fundamentals of the business and the financing mechanisms are lined up to produce a strong return on your invested cash.

Begin Due Diligence

Now that you have a signed LOI, it’s time to kickoff your own due diligence process.

The idea is to simply cover your bases.

How you do this will be determined by the things you tend to pay most attention to.

Of course, everyone tends to look at the high level fundamentals, but someone with, say, a marketing pedigree is likely to deep-dive into the marketing stack of the product with which they’ll be expect to grow revenue moving forward.

Every CEO has their own style, and there is no good way to do things. But your style will influence your due diligence.

Strategic Diligence

Perform a strategic interview in which the founding story is shared, the product vision is recalled, the market share is explained, and the overall positioning of the product relative the rest of the market and competitors.

By the end of this meeting, I should have a clear understanding of what the value prop is, how it fits into the market’s pain points, what the business model is, what the channels are, and how everything comes together to produce the growth equation.

I seek to understand what the product is for customers and where on the totem pole the product finds itself, can eventually go. I seek the product’s strengths and weaknesses.

Competitive Diligence

By understanding the market a little bit more, I can dive into the competitors and seek to understand how, if at all, they impact the greater opportunity.

Get a grip on feature parity and get a rough competitive matrix together, the purpose of which is to keep track of what positioning the product must continue to defend, or fight to secure.

Revenue Diligence

I qualify the revenues from the payouts file a second time (i.e. updated payouts) and verify that the direction of the business hasn’t shifted.

Deep dive into the cost profile of the product, from OpEx to sales and marketing. Find out how lean the operation is and whether there is space to instantly improve.

Demand Generation Diligence

Paint the picture of how the product builds demand for itself. Understand the user acquisition channels that are demonstrating strong market/product-fit.

Interview the sellers on their experience marketing and driving leads for the product. Ask how they would grow if they wouldn’t sell, quantify the cost of acquisition and baseline that relative to the reported lifetime value

Support Diligence

Take some time to talk to customers. In the absence of that opportunity, since it’s not always possible, read up on previous support tickets and/or Live Chat sessions.

My goal in this part of the diligence is to gauge NPS and identify which parts of the product are creating the most support burden and friction in the way of conversion.

Further to that, get an idea of the week-on-week support burden for as long as can be reported against.

Process Diligence

Every team has a run-of-business; a set of activities that help produce results and deliverables, externally or otherwise.

It’s crucial to understand and document how the seller is currently running the business, so you can:

Maintain the product’s momentum post-sale

Pattern find any gaps in the way things are done

Make educated workflow design choices taking into account the seller’s previous experiences

Here, I seek to understand how things are done so I can pick up the torch on closing day and confidently move forward.

Technical Diligence

By the time the transaction is nearing a close, we’ll do a non-recorded Zoom session in which the seller goes through the code-base at a high level, describing the main flow of the application, its stack, and how it all fits.

There’s no need to go in too deep, but it is worth going over some of the core functionality so as to get an idea of the code quality and likelihood that you’ll be able to pick up from where the seller left off without too much trouble.

Confirm Offer, Multiple & Expected Returns

If the starts align, your due diligence will excite you even further about the opportunity, providing evidence that the presented opportunity is in fact qualified, and that zooming into details reveals that the opportunity’s qualification is justified and has merit.

In the event of some discrepancy, this is the stage at which the offer is revised. Unfortunately, it sort of resets the whole process to LOI, minus the already performed diligence.

Confirm closing date

Granted any details related to your financing, and any timing potentially affecting it, you’ll now have enough information to set a tentative closing date you can confirm with the seller.

Pick a day and fully block it. No distractions.

Confirm terms of consideration

At this point, the terms of the transaction are confirmed and sealed, ready for use in the official asset purchase agreement.

Confirm + kickoff any financing vehicles

If you’re financing externally, now’s a good time to get in touch with your lender and share details about the transaction.

I don’t like getting in touch too early because things tend to move fast when they do. There’s no value to giving context about the deal to my broker if I’m not ready to move.

If you’re going all-cash, this might be the moment to move and allocate your funds into whatever checking account you’ll use to send your wire.

Prepare APA Template

As you go through diligence, several items to consider or cover will come up. Keep your laundry list so you can go over it, in detail, in the asset purchase agreement.

One of the most obvious ones is training. What is the agreed training period? How long will it last? When will it begin?

Take your entire laundry list of terms and conditions and codify them, as best as you can, in numbered point form.

This should give your lawyer everything they need to adjust your verbiage so you’re still saying what you’re trying to say but you’re saying it in a manner that is defensible and protecting of both parties.

Send APA to lawyer for once-over

Self explanatory — today, I have a pretty standard APA template that I re-use. I paid my lawyer once to produce a generic “mother” template, and I have several approved variations for different types of transactions.

This process can be pretty variable, both time-wise and financially. Don’t skimp. If you can get yourself a solid template you can duplicate without putting yourself in danger, that will both accelerate your process and save you money.

Send APA via PandaDoc

When approved by your lawyer, expedite the APA to the sellers. Use PandaDoc to define the text input and signature boxes for the sellers and yourself to fill in.

Receive signed APA

Congratulations! You’ve got a signed deal!

At this juncture, the transaction is sealed and approved and scheduled for closing date. Both the buyer and seller now have a list of to-do’s before and on closing date to finalize the transaction.

Final Review

I like to do a call with the seller to review that list of to-do’s and create a shared task list. That will include asset transfers, diverse accounts to share, training topics and booking them into the calendar, and so on.

By closing date, both buyer and seller should know exactly what is going to happen on closing and post-closing.

Create escrow.com transaction

With the transaction ready to go, I usually turn to escrow.com as my go-to way to pay. I also am totally fine paying in Bitcoin or Ether since that saves literal thousands of dollars in fees.

For crypto based transactions, especially future ones, I’m going to invest in a Solidity-based smart contract that can act as a decentralized escrow service between myself and sellers.

This way, provided I have proof the smart contract was audited as safe and valid, the sellers would not need to trust me to send over cryptocurrency after receiving the assets.

Otherwise, escrow.com is an absolutely fantastic way to conduct transactions. It’s fast, relatively cheap, and efficient.

I tend to do domain transfer sales, which rely on the seller attaching the domain of the product to the transaction, which means the transaction triggers once the domain is confirmed transferred.

Fund escrow.com transaction

Between 3-5 business days before closing date, use the details provided by the escrow to fund the transaction and validate it.

At this point, the seller will receive a notification that the funds have been secured, and the transaction can now take place. The ball is in the court of the seller to perform the asset transfer in closing date.

Closing date

Congratulations, today’s the day! Since you’ve already done your part, you’re merely on the receiving end.

How the asset transfer goes should already be determined.

For Reconcile.ly, which is a Shopify app, the process involved getting in touch with Shopify Partner Support and informing them that the app should be transferred to another Partner account.

That partner account (the buyer) then received an email from support requesting confirmation that you do in fact wish to receive the transferred application into your account.

Asset transfer

At the scheduled time, the assets will be transferred in your name, to your email, and so on, and you’ll officially take over ownership of them and any supporting assets.

Namely, as the domain itself gets transferred and confirmed, the escrow.com transaction confirmation will transfer over to the buyer, who now has to release the funds.

In the case of Reconcile.ly, the asset transfer was completed when Shopify sent over a confirmation of the app ownership transfer.

Fund release

As quickly as you can after confirming asset transfer, release the funds to the buyer as agreed.

This may be different from case to case. You may have an agreement to only release 25% on closing date, or you may releasing a 70% down, with the rest being an agreed upon cash balance.

Either way, the transaction’s up-front consideration is released and the acquisition is certified-complete.

Begin operations

Congratulations on your acquisition!

Hopefully you enjoy your training period with the seller. Pay close attention and record everything. They won’t hesitate to bill you for any additional consulting or advice beyond the agreed-upon training time.

Being a microangel requires speed, agility, consistency and resilience. Most of the qualities required of sales professionals, because the two disciplines share a lot of DNA.

I’ve yet to speak to a newsletter subscriber interested in being a lazy investor. Most want to influence their outcome and be deliberate about it, and aggressively pursue it once it is given a name and identity.

Unfortunately, if you’re haphazard about your approach, skip steps, or make unhealthy assumptions throughout the way, you’ll create a risky foundation upon which to acquire.

Always assume you don’t have all of the available information. On that assumption, you should adopt the stance that any information you can get your hands on should be duly analyzed for any insights that can better indicate whether you should move forward.

In the hopes that this process helps you and anyone else materialize their dreams of freedom & profit!

Till next time.1

PS. I have a favor to ask.

The MicroAngel newsletter has been an awesome experiment so far.

Building in public is cool, and I get a lot out of it, but I must say it pales in comparison to the impact and new relationships I create with subscribers along the way.

I’ve been thinking about the most efficient way to keep the newsletter valuable while being able to justify amping up research and production, do interviews, podcasts, and so on.

What I’m likely going to do is transition to a model where I release one free post every month, and the rest are for subscribers. I’d love your feedback on that. Let me know.

Thanks to the following Newsletter Sponsors for their support:

MicroAcquire, Arni Westh, John Speed & the many other silent sponsors

Hi Eyal, Absolutely loved this 'from first touch' series.

You mentioned in another post a large percentage of your dealflow comes from directly messaging founders. I wondered if you would be kind enough to share how you cold approach founders who haven't actively listed their businesses for sale.

That would be an amazing premium content addition

Best,

Sam

Great stuff as always! Quick question: when you take over a new product like reconcile.ly, are you using ARPU / churn to compute LTV? Or are you averaging out historical data of how long users stay on as paying? Thanks!